Top Ten Investment Themes for 2025

Happy New Year, everyone! As you may recall, our overall macro theme for 2024 was “An Expansion of the Rally.” The theme ultimately proved to be accurate, as the dominance of the “Magnificent 7” stocks (Nvidia, Apple, Microsoft, Amazon.com, Alphabet, Tesla, and Meta Platforms) dissipated during the second half of the year as the other “Not So Magnificent 493” stocks (i.e., the remaining stocks of the S&P 500 Index) took over the leadership role. The “Magnificent 7” accounted for 62% of the total return of the S&P 500 in 2023 and 59% during the 1st half of 2024, but just 9.20% during the 3rd quarter of 2024. This passing of the baton is important, healthy, and constructive for the continuation of the current bull market run, which is now over 2 years old, with a cumulative return of 74.22% as of November 29, 2024. For perspective on this front, prior to the current bull market, according to data from Yardeni Research and Yahoo! Finance, there have been 12 bull markets since 1946, and the average duration of those bull markets was 5.3 years, with an average cumulative return of 177.5%. Of course, this time could be different, and past performance is not indicative of future results.

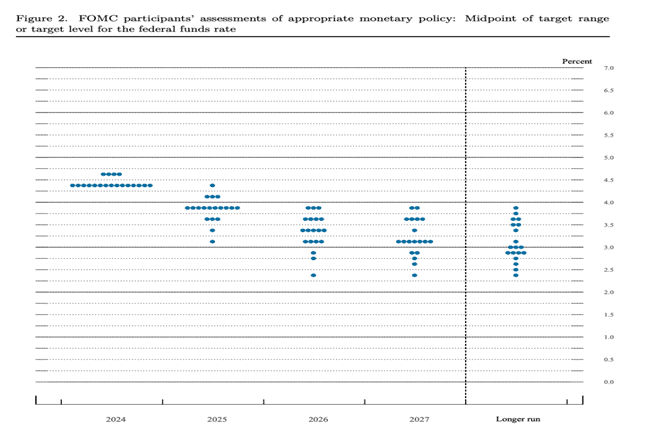

Stock market leadership was not the only significant transition that took place in 2024. The U.S. election concluded with a transition in the White House and Senate as the Republicans now control all three legs of the federal government stool, given that they also maintained control of the House of Representatives. Time will tell what this transition will mean in terms of policy implementations and their impacts on economic and stock market growth. The Federal Reserve (“Fed”) also transitioned from an inflation-fighting, higher interest rate environment to the beginning stages of what will likely be a multi-year rate-cutting campaign. They kicked off the campaign with 100 Bp (1%) in rate cuts towards the latter stages of 2024. According to the Fed’s final 2024 release of their infamous “Dot Plot” chart in December, they are forecasting another 50 Bp (0.50%) in rate cuts in 2025 and 50 Bp (0.50%) in rate cuts in 2026. The Fed is also forecasting inflation, as measured by Core PCE, to decrease to 2.5% in 2025 and then decrease further to 2.2% in 2026.

As a result, we see the theme for 2025 as “Growth Opportunities Ahead.” This theme does not imply that all areas of the market will move higher in the New Year because they likely will not. It also does not mean the economy will experience exponential growth because it likely will not. Finally, it does not imply that periods of short-term bouts of volatility will not happen, as they likely will, given current valuations and the many geopolitical and central bank uncertainties that lie ahead. What it does suggest, however, is that the next four years will undoubtedly look very different than the prior four years, and the next decade will look very different than the last decade. Over the shorter term, the outlook for lower interest rates and inflation, coupled with expected economic growth and stability under a Trump Administration (with the support of Congress), provides tailwinds for potential growth opportunities in both equities and fixed income. However, while we see numerous growth opportunities ahead in 2025, investors would be wise to be selective as growth will likely be less than what the stock market experienced in the prior two years and more pronounced in certain areas of the market than others. We highlight some of these areas below.

Here are our “Top 10 Investment Themes for 2025″ for your review and consideration.

1. Bull Market and Earnings Growth Expansion

For the breadth of the bull market to continue to expand, the breadth of the earnings rally also needs to expand. Fortunately, both of these expansions began during the 2nd half of 2024, and we believe that the momentum will carry forward through 2025. In terms of earnings growth, according to FactSet, the per-share operating earnings growth pace for the overall S&P 500 Index is currently forecasted at 15%. As a result, expanding beyond, but not necessarily abandoning, U.S. large-cap stocks is worthy of consideration for the New Year. Expansion candidates would include U.S. mid-cap, U.S. small-cap, and international stocks (predominantly international developed market stocks) that pay attractive dividends, have a history of price performance, and are poised for total return potential ahead.

2. The Long Game of Artificial Intelligence Investing

In terms of where we are in the timeline of artificial intelligence (AI), I believe that we are just in batting practice of a double-header with so many more opportunities that lie ahead in the development and application of AI. According to Faist, as of June 11, 2024, the global AI market is expected to reach $1.81 trillion by 2030, with a 36.6% compound annual growth rate (CAGR). However, investors and companies need to be patient with their investments in this revolutionary technology, as some may not necessarily see a return on their investment for years to come. As we see it, the AI revolution road is a long one with many potholes that will create many winners and many losers. As a result, as opposed to just trying to find the next Nvidia or hot chips/semiconductor company, investors should consider potential investment opportunities in the entire AI Ecosystem, which is comprised of data centers, software, hardware, and chips/semiconductors. Data centers and their associated tremendous need for power and cooling solutions, in particular, have become a critical component of the AI ecosystem.

3. Increased Investment in Defense and Security

U.S. defense and national security needs to focus on replenishment, upgrades, and modernization, addressing gaps in naval readiness, advancing missile defense systems highlighted by recent conflicts, and integrating cutting-edge technologies like autonomous systems (ex. drones) to meet evolving global threatsFortunately, more spending is on the way as defense spending in the United States is predicted to increase every year over the next decade, totaling approximately $1.1 trillion in 2034 – that represents an increase of over 20% vs. 2023 and 263% vs. 2000, according to Statista Research Department as of July 5, 2024. Companies that play a pivotal role in areas such as enhancing military readiness, advancing missile defense systems, and driving technological innovation in autonomous and defense technologies stand to benefit from the increases in investment and spending in these areas.

4. Fed Adopts More Gradual Pace toward Interest Rate Cuts

According to their updated Dot Plot chart (see below), the Fed is currently forecasting 50 Bp in additional rate cuts in 2025 and another 50 Bp in rate cuts in 2026. All of this would follow the 100 Bp in rate cuts that the Fed enacted during the latter stages of 2024. These cuts align with their long-run neutral rate expectation of around 3.0%. In terms of the pace of their cuts, we believe that the Fed will adopt a more gradual pace of easing in 2025 and 2026 with no single rate cuts of greater than 25 Bp until the Fed Funds Target Rate is closer to their long-run neutral rate expectation of 3% (which may not be achieved by the end of 2026), given the many uncertainties surrounding the labor market, inflation, potential tariffs, and the policies to be implemented by the incoming administration. Regardless of the pace and extent of this rate-cutting campaign, it has become abundantly clear that interest rates will be lower in 2025 and over the next two years. As a result, investing in areas of the market likely to benefit from a declining interest rate environment is worthy of consideration. These areas may include, but are not limited to, certain sectors of equities, such as Health Care, Information Technology, Consumer Staples, Financials, Communication Services, and Consumer Discretionary, as well as bonds of different credit qualities, with an overweight towards investment grade.

Federal Reserve “Dot Plot” Chart as of December 18, 2024

5. Large Cap Pharma Turns to Small Cap Biotech for Answers

Large-cap pharmaceutical companies face multiple headwinds as they continue to have their profit margins pressured by Washington DC’s push to lower drug prices and larger revenue-producing drugs that have come off patent or are scheduled to see come off patent and be challenged by lower generic drug prices. One answer to their revenue quandary can be found in the innovative healthcare solutions being developed by smaller-cap biotech firms. These innovative healthcare solutions, which are now being assisted by artificial intelligence developments in certain cases, include but are not limited to gene therapies, RNA therapeutics, precision and target oncology treatments such as CAR-T cell therapies, and, of course, obesity drug breakthroughs such as GLP-1. In 2024, according to BioPharma Drive, as of November 26, there were 36 Biotech M&A transactions totaling just over $45 billion, the latter well below expectations coming into the year as many of the deals involved smaller companies. However, the average premium paid for the 36 transactions in 2024 was an impressive 83%. Looking ahead to 2025, many analysts are optimistic that the total number and total $ amount of biotech-related M&A transactions will increase. To this end, PwC, in their “Pharmaceutical and life sciences: US Deals 2025 outlook,” expects transactions between $5 billion and $15 billion to see sustained activity in 2025 while recognizing geopolitical factors that could bring headwinds. Investors thus need to find those smaller-cap biotech companies with existing breakthroughs or innovative drugs in the FDA approval pipeline that large-cap pharmaceutical companies desire to add to their platforms and thus have the greatest chance of being acquired. Small-mid cap biotech companies with strong pipelines and focused therapies, such as rare diseases, RNA-based therapies, or advanced immunology, according to Biopharma Boardroom, appear to have the most appeal to potential Large-cap pharmaceutical acquirers in the current environment. Looking for those companies with related drugs in Phase II or Phase III of the FDA approval process is a good starting point for identifying potential investment opportunities.

6. Munis Poised to Perform

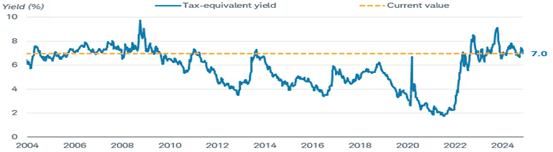

Tax free income is always attractive to income-oriented investors, particularly investors in higher tax brackets. We anticipate this level of attraction being heightened in 2025. Heading into the New Year, the balance sheets of many local and state governments are relatively strong, and the positive outlook for employment and the economy in 2025 should bode well for the tax revenues of many municipalities. Additionally, comparable yields of Municipal Bonds (Munis) are currently, and should remain, very attractive to investors. According to data from Schwab, the tax-equivalent yield of Munis for an investor in the top tax bracket is near its high over the past 15 years (see chart below).

Source: Schwab, Bloomberg Municipal Bond Index, as of 12/3/2024. Assumes a federal tax rate of 35% from 2004 to 2012, 39.6% from 2013 to 2017, and 37% from 2018 to 2024. Also assumes an additional 10% state income tax and 3.8% Net Investment Income (NIIT) tax. Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. Past performance is no guarantee of future results.

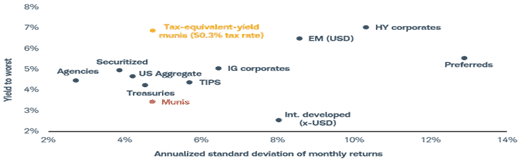

These taxable equivalent yields become even more appealing after factoring in the risk (as measured by standard deviation) of the various fixed income asset classes when compared to Munis, as depicted in the chart below from Schwab.

Concerns over the potential repeal of the municipal bond exemption appear now to be overblown, setting the stage for what could be a high level of demand for municipal bonds and municipal bond-oriented strategies in the New Year. Lower short-term interest rates should also benefit municipal closed-end fund (CEF) strategies that employ leverage, many of which are still trading at a discount to their net asset values (NAVs).

7. Financials (including Regional Banks) Rebound

Many of the factors that led to the regional banking crisis and ensuing hangover have seemingly abated as short-term interest rates have declined (and are forecasted to decline further), the prices of U.S. Treasuries have increased, and the prospects for more economic growth and less regulation have increased following the election of Donald Trump. Less regulation and lower potential capital requirements could also lead to great industry consolidation via an increase in mergers and acquisitions (M&A). To this end, Piper Sandler analyst Mark Fitzgibbon said in a Banking Dive article that he expects 2025 and 2026 to see robust bank M&A activity and that deal approvals, under a Trump administration, will speed up markedly and the process will be more clearly delineated. Regional banks rebounded during the latter half of 2024. We believe that the rebound will extend, and more potential upside remains for certain regional banks in 2025.

8. Preferreds Benefit from Financials Rebound and Lower Interest Rates

Preferred securities (Preferreds) represent ownership in a corporation and have both bond and stock-like features. Preferreds generally pay a fixed income, have a par value, hold a credit rating, and trade on major exchanges. They also typically have a higher stated dividend payout than the corporation’s common shares and even bonds. Despite these features, they are often not considered by investors to help meet their respective income and growth needs, and perhaps they should be. Preferreds did suffer a pullback following the regional bank crisis that began back in March 2023 with the seizure of Silicon Valley Bank, given that banks are typically the largest issuer of preferred securities and contagion risk was at the forefront of many investors’ mindsets. However, as discussed earlier, many of the factors that led to the regional banking crisis have now dissipated, creating attractive entry points for many preferred securities that have not yet fully recovered from the pullback and potential total return opportunities ahead.

9. Look to Sources of Power to Help Power Your Returns

Data centers are forecasted to use up to 9% of total electricity generated in the United States by the end of the decade, more than doubling their current consumption, according to Reuters as of May 29, 2024. Electricity is stretched in the U.S., and our electricity grid is antiquated and unreliable. As a result, the data centers that serve as the nervous system of the AI ecosystem will need to look beyond traditional energy sources, such as electricity, and alternative sources of energy, such as natural gas and nuclear energy, to help provide the massive amount of power they need. As it relates to natural gas, S&P Global Ratings estimates that U.S. data centers’ increasing energy demands will lead to additional gas demand of between 3 billion – 6 billion cubic feet per day by 2030, from a starting point of almost none today. As it relates to nuclear energy, Goldman Sachs believes that we are in the early stages of a nuclear renaissance in the U.S. and globally as it relates to data center power demand in the form of small modular reactors (SMRs) and larger-scale nuclear power plants. Companies that provide products or services in these areas stand to benefit from all of this anticipated demand for power in the new year.

10. Expect More Short-Term Bouts of Volatility but Don’t Abandon Stocks

In 2024, as of December 2, there were only 16 days where the S&P 500 Index moved by more than 1.5% in a given trading day – and 7 of those 16 days were positive moves! This amount translates to just 3% of the trading days involving a downside move of 1.5% or more, representing a historically low level of volatility and should not be expected to continue throughout 2025. The S&P 500 also saw 54 record closes in 2024, as of December 2, so valuations are rich, and smaller-scale corrections are possible. These corrections, of course, can be met by money coming off the sidelines to take advantage of more attractive entry points. The potential for more volatility in 2025 does not mean that investors should try to time the market, as timing the market is often an exercise in futility, and “staying on the sidelines” for too long can have a negative impact on achieving longer-term financial goals. Rather, a more balanced approach towards stock market positioning, perhaps through equal-weighted strategies, covered calls, or more defensive stocks, may be worthy of consideration for certain investors and/or portions of their overall portfolios.

Let Hennion & Walsh Offer a Second Opinion

Curious to learn more? Our unmatched client experience will give you peace of mind. Just as you may seek a second opinion about your health, we believe successful investors can gain value and peace of mind by getting a second opinion on their financial health. So, whether you’re worried about today’s uncertain economic environment or looking for increased peace of mind, we can help. Get a complimentary second opinion on all your investment accounts not held at Hennion & Walsh today!

Hennion & Walsh Experience

At Hennion & Walsh, every client, every individual investor, is assigned a dedicated team of investment professionals, planners, and portfolio managers, who collectively analyze your situation through the lens of their respective disciplines.

Each member brings valuable insights to apply to your situation. Whether you’re looking to meet your income needs today or stock market growth for your future, we have an expert sitting with you, helping you, and guiding you through all the scenarios to help you live the life you want.

Hennion & Walsh distinguishes itself in the investment industry with its exceptional in-house team of specialists committed to your success. Unlike other firms that rely on impersonal call centers, Hennion & Walsh provides direct access to experienced bond experts, CERTIFIED FINANCIAL PLANNER (CFP®) professionals, Chartered Financial Analyst (CFA)® charterholders, annuity professionals, and a proficient internal fixed-income trading team. Our customer service team is exceptional, ensuring that every client receives the dedicated attention and support they deserve.

Disclosures:

Hennion & Walsh Asset Management currently has allocations within its managed money program, and Hennion & Walsh currently has allocations within certain SmartTrust® Unit Investment Trusts (UITs) consistent with several of the portfolio management ideas for consideration cited above.

Investing involves risk, including loss of principal. To determine if a Trust is an appropriate investment for you, carefully consider the Trust’s investment objectives, risk factors, charges, and expenses before investing. This and other information can be found in the Trust’s prospectus, which may be obtained by calling 1-888-505-2872 or visiting our website at www.smarttrustuit.com. Please read it carefully before investing.